Publish Date

May 22, 2016

Region: North America

In the years following the financial crisis, the U.S. financial services industry has weathered a myriad of economic and regulatory challenges which negatively impacted performance, constricted liquidity and hampered deal activity. With continued economic improvement, technology enabling differentiation, and strengthening fundamentals across the financial services sector, deal activity has seen a continued upward trajectory through the end of 2015. In fact, financial services M&A activity reached its highest peak in 2015 compared to any point over the last 10 years.

KEY 2015 M&A TRENDS

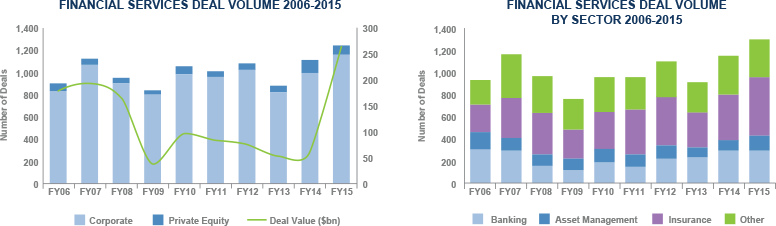

There were a total of 1,267 financial services deals in 2015, with an announced deal value of $264 billion. The number of deals with a value over $1 billion (i.e., “mega-deals”) also reached a peak in 2015, with 35 deals representing $233 billion or 88% of total announced deal value.

• Although there has been a marked increase in the pace of banking deals since the financial crisis, (excluding government-assisted transactions), recent deal activity remains somewhat flat. There were 285 deals in 2015 representing $27 billion of announced deal value. While five mega-deals accounted for $14 billion or 54% of announced deal value, the majority of transactions related to consolidation amongst banks with less than $1 billion in assets.

• There were 331 deals in 2015 in the other (non-bank) financial services sector, with an announced deal value of $91 billion. This includes a record 19 mega-deals representing $79 billion or 87% of the total announced deal value. Financial technology and specialty finance transactions dominated this segment, representing a total of 259 deals and 86% of the total announced deal value in 2015. Pervasive and continued advancements in technology will drive substantial growth in financial technology deals, spanning the financial services spectrum. Expect sustained mid- to high-teen deal multiples for innovative firms with a proven track record of high quality growth.

• Insurance represented the most active financial services subsector, with 521 transactions representing an announced deal value of $143 billion. While 451 insurance brokerage deals represented 87% of insurance deal volume, they only accounted for around 2% or $3 billion of announced deal value. Insurance underwriter acquisitions by strategic acquirers accounted for the lion’s share of announced deal value.

• Asset management deal activity remains robust, with 130 deals in 2015, compared to 91 deals in the prior year. Average deal values for announced asset management deals, excluding mega-deals, appears to have declined from $108 million to $88 million over the same period. While deal activity remains strong, the decline in pricing likely reflects the impact of recent financial market volatility on valuations, narrowing the bid-ask spread between buyers and sellers.

Focused growth: A bigger role for private equity

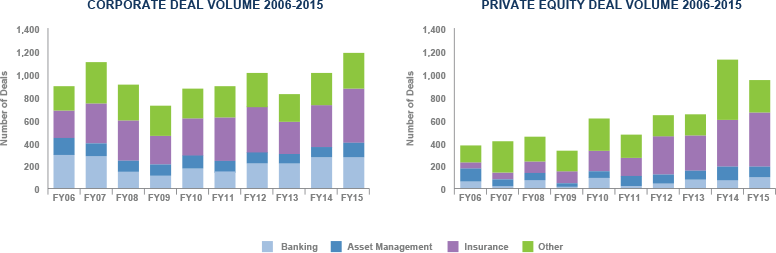

Although private equity deal activity has tripled since its low point in 2009, financial services M&A remains dominated by corporate buyers. Corporates represented 1,169 deals with a disclosed deal value of $252 billion, compared to private equity investors, which represented 98 deals with a disclosed deal value of $12 billion. While corporates will likely continue to dominate larger, balance sheet-heavy deals in more-highly regulated subsectors, private equity firms will play an increasingly dominant role in deals involving commercial lenders, specialty finance companies, financial technology firms, insurance brokerage firms, and asset / wealth managers.

Of the 98 private equity deals announced in 2015, 48 related to insurance brokerage, 16 related to financial technology and six related to specialty finance transactions. These three subsectors accounted for over 71% of all private equity-backed deals in 2015. We believe these three subsectors will continue to represent the most significant areas for investment by private equity firms.

DISRUPTION AND EVOLUTION: KEY TRENDS TO WATCH

Continued improvement in the U.S. economy, characterized by sustained GDP growth, declining unemployment, historically low interest rates, lower energy prices and growing consumer confidence, gave buyers and sellers the confidence to push forward with deals in 2015. While recent financial market volatility and global economic concerns have tempered growth expectations in the near-term, we believe the pace of financial services deal activity will persist.

We believe the following key trends and themes will drive M&A activity across the financial services sector over the coming years:

• The impact of technology is pervasive, from the use of big data to understand customer behavior and improve underwriting, to driving new customer and asset acquisition. Growth in emerging collaborative technologies such as blockchain are already impacting recordkeeping and transaction processing capabilities across the financial services sector. Continuous disruption and disintermediation by technology-enabled market entrants will spur innovation and deal activity.

• Regulators will continue to play an integral role in the banking, insurance and consumer finance subsectors, intensifying their interactions with incumbents and new entrants. While uncertainty over the extent and nature of regulatory oversight remains, savvy investors will look through the regulatory white noise and seek to execute deals rather than wait on the sidelines for future clarity.

• The largest financial institutions will continue to divest non-core businesses while competing aggressively with new entrants for growth; expect growth in deal activity as incumbents seek to use their considerable capital to acquire knowledge and market share.

• Innovation and investment will be drawn towards business models that are scalable, highly data intensive and capital light.

• The proliferation of financial services offerings for the nonprime and underbanked segments will continue. Technology will increasingly enable more efficient and effective underwriting, streamlined processing and servicing, and disintermediation across the sector.

• Scale from consolidation will become critical for an increasingly commoditized financial services sector; growth from the realization of cost synergies and footprint / product expansion will continue to spur deal activity.

• Challenging organic growth opportunities and a historically low interest rate environment means new asset generation remains difficult. The inevitable, albeit measured increase in interest rates, will enhance lender profitability, increasing their attractiveness to investors.

• While historically less prevalent compared to other industries, expect activist investors to play an increasingly active role in driving M&A activity across the financial services spectrum.

CLOSING THOUGHTS

The pivotal role of technology is giving rise to structural changes across the financial services sector. As the industry adapts and evolves, M&A activity will play a continued role in this growth story. Investors who understand the impact of key risks and drivers of deal value at the most granular level will be in a position to execute the most successful transactions. A robust and deeply analytical diligence process by sellers and buyers will be of critical importance to ensure that contingencies, synergies and risks are identified and quantified before the consummation of a potential transaction.