Publish Date

Nov 06, 2019

There are several areas of deal risk to consider when evaluating the earnings quality of a healthcare services target. This article is the first in a series of articles that will illustrate the comprehensive way we analyze the most significant elements impacting a healthcare target’s earnings.

The Importance of Revenue Recognition in Healthcare

Patient services revenue is both the biggest number driving EBITDA and the hardest number to record accurately for healthcare CFOs. As you explore investment opportunities with healthcare services targets, you and your advisors should take a rigorous and thoughtful approach to assessing revenue quality. We frequently see examples of advisors addressing patient services revenue in a “light touch” manner in the marketplace. Make no mistake, “trimming the treetops” when assessing patient services revenue recognition is a valuation miss waiting to happen.

Why is Healthcare Revenue Recognition Challenging?

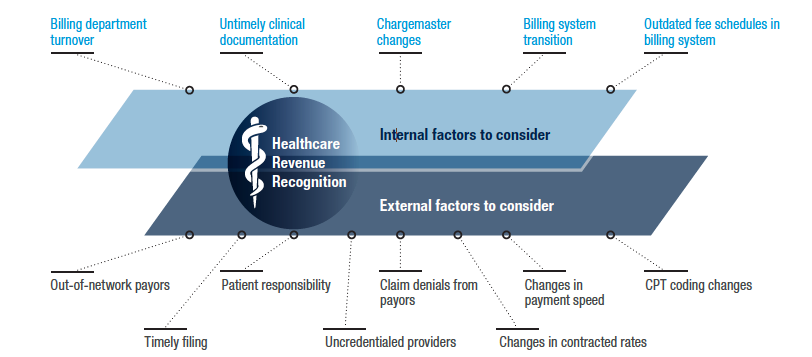

When a healthcare CFO records revenue, they are estimating cash collections that will be received in the future for services rendered during the current period. However, the payment mechanisms through which claims are adjudicated by third-party payors are complex and include both payor and patient obligations. Numerous internal and external factors must be considered when recording revenue, as illustrated below.

Even for the most seasoned healthcare CFO, healthcare services revenue recognition can be challenging. Accordingly, the risk that reported revenue is materially misstated in a healthcare target is relatively high. This is why we spend much of our time in diligence assessing such matters.

How Do We Assess It?

Our approach is comprehensive and multi-faceted. We assess a target’s revenue quality by building an independent view of accrual basis revenue and comparing that view to the target’s comparably recorded revenue. The difference often directly impacts earnings and has significant implications for enterprise value.

Our process starts with obtaining granular data sourced directly from a target’s billing and collections platform, including both chargesand collections, generally at the claim and CPT code level, by date of service.

After we gather this data, our data integrity checks are then completed. These are critical because any revenue quality analysis is susceptible to “garbage in, garbage out”—inaccurate data will lead to inaccurate conclusions. We reconcile (i) charges on a date of service basis to existing reports that have historically proven reliable and (ii) cash receipts to bank statements to ensure they are complete and accurate. Getting accurate data and reconciling it successfully is often the heaviest lift in our analysis, requiring multiple turns of information and significant effort. This step is also one we see most commonly skipped in the marketplace, likely due to the level of effort required.

After obtaining the data and confirming its integrity, we analyze the target’s collection patterns, bifurcated by relevant payor and modality groupings, or other relevant cuts, to understand trends in both collection rates and speed. Equally important, we spend significant time with the target’s revenue cycle management function, discussing key element such as:

This qualitative knowledge is then combined with the quantitative information gathered from our detailed claim and CPT-code level waterfall analysis to create an independent estimate of accrual basis patient services revenue.

What Are the Implications of Our Analysis?

The major implication of our analysis is how it impacts EBITDA. This is determined by comparing our independent view of revenue to the income statement and calculating how the difference impacts earnings. Offsetting considerations may exist that dilute the earnings impact of the revenue difference, the most common being situations in which providers are paid as a percentage of revenue or collections.

It is also important to understand why differences exist between our independent view of revenue and the target’s financial statements. Sometimes the difference is simply due to the target maintaining cash basis financial statements as compared to our view of accrual basis revenue. In other instances, understanding the difference between our view and the target’s view of revenue can uncover hidden flaws in the target’s revenue recognition methodologies or, more importantly, revenue cycle weaknesses. Awareness of such flaws is the first step towards remediation under our client’s potential ownership.

What’s Next?

Stay tuned for the next article in this series that discusses the business diligence learnings that result from our Quality of Revenue Analysis. We like to refer to such learnings as the “Quality of the Revenue.”

Key Contacts: