Publish Date

Jun 14, 2018

Region: Asia

Paul Aversano and Xuong Liu, managing directors of Alvarez & Marsal, comment on the impact of US/China trade tensions on cross-border M&A – specifically what it means for the UK.

Given everything that has taken place in the world over the last couple of years, it’s perhaps unsurprising that the M&A market looks markedly different today than it did in 2016.

Back then, Chinese capital was pouring into North America and every deal seemed to be defined by a Chinese bidder on the other end. With the almost daily onslaught of news describing souring US/China trade negotiations, that now feels like a distant memory.

But the consequences of a dramatic shift in China/US relations for M&A spread further than the US coastline. For European professionals, there are also significant changes afoot – albeit of an entirely different kind. While the Chinese money in the States has now slowed significantly, European M&A is booming, fuelled by the same bidders who once had their eyes on American deals.

When trying to understand what has caused the money to flow in a different direction, it’s easy to jump to the conclusion that this is a trade issue alone. Donald Trump’s campaign promises (and the translation of those promises into actual policy) are clearly causing uncertainty which is scaring off bidders. But underneath a lot of the noise and, largely unwarranted, talk of a ‘trade war’, there is the reality of ever-tightening regulation when it comes to inbound M&A.

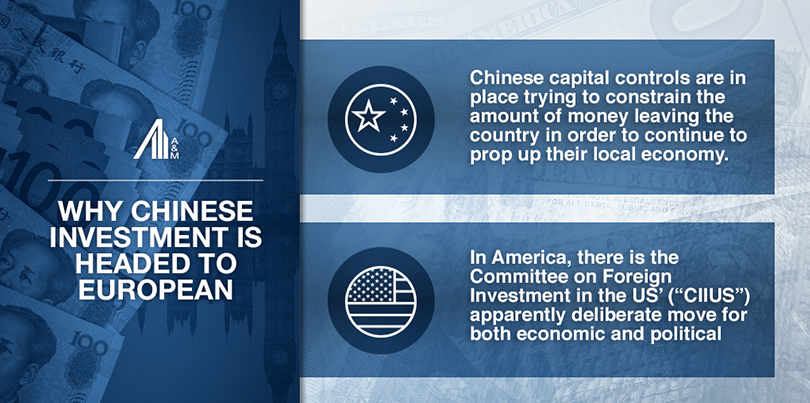

What is taking place now is a dual effort on both the part of the Chinese and the US to reign in previous levels of spending. On the one hand, Chinese capital controls are in place trying to constrain the amount of money leaving the country in order to continue to prop up their local economy. In America, there is the Committee on Foreign Investment in the US’ (“CIIUS”) apparently deliberate move for both economic and political reasons to slow down deals involving foreign capital – and President Trump is going so far as to propose regulations to strengthen even further the purview of CFIUS. With the Trump administration also suggesting that China has engaged in IP theft for many years, it’s clear that the States no longer looks as attractive as it once did.

Adding to this is the growing appeal of the European market. As well as the absence of what one may consider a hostile trade policy, European M&A regulation is currently far more welcoming to outside investors like China. Though there’s been talk of the EU beefing up its regulatory rules around foreign investment, the various players are currently too preoccupied with their own matters at home to adopt a unified front.

The political landscape is also much more attractive. Initial fears that Brexit would dry up outside investment seem to be largely unwarranted, at least for now. Unless it is set to directly impact a specific transaction post-Brexit, Chinese bidders appear largely unconcerned. There’s still the unwavering need to look for technology and brands to be brought back home to elevate their companies into leading national and, ultimately, global champions. France is arguably in a better position still, with President Macron’s election and subsequent reforms sending a powerful signal abroad that the country is attractive to inbound investment. Currency stability across Europe should also stave off any potential competition from South East Asia which is becoming an ever-more popular investment destination.

Barring a radical change in approach from the US administration, the flow of capital looks set to flow towards European shores, where it will be welcomed with open arms. With a host of new bidders in town, however, investors should be warned that sky-high valuations are unlikely to change anytime soon.

Source: https://www.acquisitionsdaily.com/2018/06/12/why-chinese-investment-is-headed-to-european-shores/

Visit my site: https://www.paulaversano.com/2018/06/why-chinese-investment-is-headed-to-european-shores/

For more about our Alvarez & Marsal Global Transaction Advisory Group: https://www.alvarezandmarsal.com/expertise/global-transaction-advisory